2024-04-08 by Sue Hunt

Many people believe that estate planning is only about planning for their death. But planning for what happens after you die is only one piece of the estate-planning puzzle. It is just as important to plan for what happens if you become unable to manage your own financial or medical affairs while you are alive (in other words, if you become incapacitated).

What happens without an incapacity plan?

Without a comprehensive incapacity plan, if you become incapacitated and unable to manage your own affairs, a judge will need to appoint someone to take control of your money and property (known as a guardian of the estate) and to make all personal and medical decisions for you (known as a guardian of the person) under court-supervised guardianship proceedings. The guardian may be the same person, or there may be two different people appointed to these roles. Depending on state requirements, the guardian may have to report all financial transactions to the court annually, or at least every few years. The guardian is also typically required to obtain court permission before entering into certain financial transactions (such as mortgaging or selling real estate). Similarly, the guardian may be required to obtain court permission before making life-sustaining or life-ending medical decisions. Court-supervised guardianship is effective until you either regain the ability to make your own decisions or you pass away.

Who should you choose as your financial agent and healthcare agent?

Guardianship statutes are the state's default plan for appointing the person or people who will make decisions for you if you cannot make them for yourself. This default plan, however, may not align with the plan you would have put into place on your own. Most importantly, state statutes may give priority to someone to act as your guardian who is not the person you would have selected had you engaged in proactive planning.

Rather than having a judge appoint these important decision-makers for you, your incapacity plan allows you to appoint the trusted individuals you want to carry out your wishes. There are two very important decisions you must make when putting together your incapacity plan:

The following factors should be considered when deciding who to name as your financial agent and healthcare agent:

What should you do?

If you do not proactively plan for incapacity before you become incapacitated, your loved ones will likely have to go to probate court to have a guardian appointed. This would be a hassle, taking time and costing money during what is already likely to be a very stressful and emotional time.

Part of creating an effective incapacity plan means carefully considering who you want as your financial and medical agents. You should also discuss your choice with the person you select to confirm that they are willing and able to serve. This would also be a great opportunity to discuss with them your wishes as to the medical and financial issues that are most important to you.

Our firm is ready to answer your questions about incapacity planning and assist you with choosing the right agents for your plan.

2024-04-04 by Sue Hunt

An intrafamily loan is a financial arrangement between family members—one who is lending and another who is borrowing. An intrafamily loan may be used to help a family member who needs money for a number of reasons:

Lending to a child or grandchild can be satisfying. Your loved ones can benefit from flexible repayment terms and interest rates while learning financial responsibility. This can be beneficial if the child or grandchild would otherwise have difficulty obtaining a loan through more traditional methods. It also gives you an opportunity to add to your investment income.

How you give or loan money to family members has potential tax implications. The right method depends on your family circumstances.

An intrafamily loan might be beneficial in estate planning for wealth transfers between generations while minimizing estate tax implications. Further, by using an intrafamily loan to provide money to a family member rather than making a gift, you can maintain control over the principal amount and how it is used.

Intrafamily loans are valuable tools for preserving wealth and offer the following advantages:

Under current tax law, gift and estate taxes are not imposed on gifts up to $13.61 million for individuals and $27.22 million for married couples in 2024. While many people's net worth is not that high, intrafamily loans may be a great option for high-net-worth families.

If the family member receiving the loan invests the money and the investment returns on the borrowed funds exceed the interest rate charged, the excess growth is passed to your family member without being subject to gift or estate taxes. This strategy preserves your lifetime estate tax exemption amount as long as all of the formalities of issuing a loan are observed. However, the initial loan amount (the principal) and interest owed to you will still be included in your taxable estate because the principal and interest are legally required to be paid to you. However, as previously mentioned, the growth in the investment will not be included in your taxable estate.

You might also consider loaning the money to a trust for the benefit of your family member as part of your planning strategy. As opposed to the strategy of loaning funds directly to your family member, the loan would be made to the trust. If the rate of return from investing the loan proceeds exceeds the loan's interest rate, the excess is considered a tax-free transfer to the trust.

With intrafamily loans, you have the flexibility to set the interest rate at a level lower than commercial lenders, as long as the rate is not below the Applicable Federal Rate (AFR) (read below for further discussion on the AFR). The cost savings for the borrower can be significant. Further, if the AFR is high when you initially make the loan, it may be easier to reissue the note from you to take advantage of any future lower interest rates than it would be to refinance a note from a third-party lender.

Intrafamily loans can play a crucial role in transferring a family business from one generation to the next. By providing financing to family members who wish to take over the family business, for example, you can ensure a smoother transition and help sustain the family legacy.

Determining the interest rate for your intrafamily loan is crucial to avoid unnecessary tax consequences. The Internal Revenue Service (IRS) publishes AFRs monthly, broken down into three tiers for short-term, mid-term, and long-term rates. Rates can be fixed or variable and structured to the advantage of both parties. The minimum AFR rate must be charged for loans over $10,000 regardless of a loved one's credit rating, and it is usually lower than most commercial lenders. If the interest rate for your intrafamily loan is below the AFR, the IRS may require you to pay income tax on the income you should have received under the applicable AFR even though the borrower did not pay you that amount (called imputed interest). Also, the amount of interest you did not collect but should have may also be considered a taxable gift to the borrower, potentially reducing the amount of gift and estate tax exemption available to you.

Since the IRS generally assumes that wealth transfers between family members are gifts, it is essential to have the proper documents showing that the transfer is intended to be a loan. You and your family member must sign a promissory note that adheres to the state-specific rules to properly document the loan transaction.

A comprehensive written promissory note is crucial. It helps avoid unnecessary tax consequences and clearly communicates the terms of the loan between family members to avoid misunderstandings and conflicts.

Every financial decision has the power to strain family relationships. When trying to determine if an intrafamily loan is right for your situation, ask the following questions:

You must carefully consider the decision to gift versus use intrafamily loans, including the income, estate, and gift tax implications. The tax rules regarding intrafamily loans are complex and may result in unintended consequences if the loan is not done correctly. If you already have an intrafamily loan in place, it is important to properly document it in your estate plan to ensure that everything will proceed smoothly if you pass away before the loan has been paid back. We are happy to meet with you and your tax advisor to make sure that this strategy is right for you and your family.

2025-04-02 by Sue Hunt

Approximately three-fourths of Americans do not have a basic will.[1] Many of the same people also have children under the age of 18, which underscores a major misunderstanding about estate plans: They can accomplish much more than just handling financial assets (money, accounts, and property).

One of the most important estate plan functions for parents of minor children is the ability to provide specific guidance about how their children will be cared for and who will care for them in case something happens to the parents.

To account for all emergency contingencies concerning you and your children, your estate plan should form a comprehensive safety net that addresses your children's care needs and protects them from the unthinkable.

Three Tools You Need If You Have Minor Children

As parents, we instinctively strive to shield our children from harm and set them up for success, now and in the future.

While we cannot predict the future, we can prepare for it. Estate planning is a crucial step in this preparation, especially when minor children are involved. It is not only about distributing your money and property after your death; it is also about establishing ways to care for your children if you no longer can.

Your death or incapacity (inability to manage your affairs) from a sudden illness or accident is a situation that you would likely rather not think about but must consider in preparing for worst-case scenarios that could lead to a court deciding who cares for your child.

Data on parental mortality is sobering: More than 4 percent of minor children have lost at least one parent.[2] If you wait too long to create your estate plan, it could be too late. More than any other reason, Americans cite procrastination as the reason they do not have an estate plan.[3] Procrastinating on creating your estate plan could mean it will not be there when you—and your children—need it.

To safeguard your children's future, three estate planning tools are particularly important: a will, a power of attorney for minors, and a standalone nomination of guardian.

Last Will and Testament

A last will and testament (also known as a will) is a cornerstone of any estate plan, but it takes on added importance when you have minor children. Your will outlines your wishes regarding the distribution of your money and property after your death. It also allows you to do the following:

Power of Attorney for Minors

A power of attorney for minors, sometimes called a designation of standby guardian or something similar depending on the state, is a legal document that empowers a chosen individual (your agent or attorney-in-fact) to act for your minor child on your behalf. This person steps in to make decisions regarding your child's care if you become incapacitated or unavailable.

The power of attorney can grant the agent broad authority to handle various aspects of your child's life, including the following:

Although the power of attorney grants the agent significant authority, there are limits to what it permits. The agent cannot consent to the child's marriage or adoption. In addition, many state laws impose expiration dates on these documents (e.g., six months, one year), so it is important to review and update them regularly to ensure that they remain valid.

Revocable Living Trust

In addition to a power of attorney, nomination of guardian, and will, the parents of minor children might consider a revocable living trust that holds their accounts and property during their lifetime and distributes them after their death.

You (the parent) maintain control of the accounts and property in the trust while you are alive as the current trustee. You can change the trust's terms as needed because you are the trustmaker, and this type of trust is revocable. A revocable living trust can help avoid probate and give your children faster access to the resources they need. You can also specify how and when your children receive their inheritance, name a successor trustee to continue management of the trust if you suffer incapacity, and provide financial support for the guardian, further synergizing your estate plan.

How These Tools Work Together—and What Can Happen If You Do Not Plan

These three estate planning tools are not interchangeable; they are complementary and designed to work together to address immediate and long-term needs in a range of potential scenarios.

Imagine a scenario where both parents are in a car accident. One parent dies, and the other is severely injured and temporarily incapacitated. The agent named in the temporary power of attorney or delegation of standby guardian immediately steps in to temporarily care for the children.

If the injured parent passes away, the designated guardian (who may be the same person as the agent under the temporary power of attorney) named in the will or standalone document can provide the children with a stable permanent home. The will can be structured so that the children's inheritance is managed through a trust that specifies how and when their inheritances should be spent and distributed.

Failure to have any one of these estate planning tools can lead to complications and unintended consequences for your minor children. For example:

Other Planning Tools and Tips for Parents

Parents should understand that they can only nominate a guardian for their child, not legally appoint one; the court has the final authority to decide, though it gives significant weight to the parents' nomination.

If there is evidence that your chosen guardian is unfit or unable to provide proper care, the court may appoint a different guardian in the child's best interest, even if it goes against your wishes. There is also the chance that a family member could contest your guardianship choice or your first choice of guardian is unavailable.

These outcomes are unlikely, but since they could undermine your wishes, there are additional steps you can take to minimize the risk and strengthen your case.

Fitting Together the Pieces of Your Estate Plan

Each part of an estate plan has a role to play, but they work best when considered as parts of a larger plan that addresses big issues such as the well-being of your minor children.

A will, temporary power of attorney, and standalone guardian document are not interchangeable; they are complementary. Incorporating all three into your plan, alongside other strategies such as a revocable living trust and a letter of intent, addresses the immediate and long-term needs of your minor children in any eventuality.

If you have minor children, estate planning is a necessity. Do not leave your children's future to chance. Consult with us to create a multipoint plan that protects you and your family.

[1] Victoria Lurie, 2025 Wills and Estate Planning Study, Caring (Feb. 18, 2025), https://www.caring.com/caregivers/estate-planning/wills-survey.

[2] George M. Hayward, New 2021 Data Visualization Shows Parent Mortality: 44.2% Had Lost at Least One Parent, U.S. Census Bureau (Mar. 21, 2023), https://www.census.gov/library/stories/2023/03/losing-our-parents.html.

[3] Lurie, supra note 1.

2024-04-04 by Sue Hunt

Probate is the court-supervised process of either (a) carrying out the instructions laid out in the deceased's will or (b) applying state law to distribute a deceased's accounts and property to their family members if the deceased did not have a will. The main purpose of the probate process is to distribute the deceased's money and property in accordance with the will or state law. Not all wills, and not all accounts and property, need to go through probate court. And just because a will is filed with the probate court does not mean a probate needs to be opened. But whether or not probate is necessary, most state laws require that a will be filed when the creator of the will (testator) passes away.

Estates, wills, and probate are distinct, yet interrelated, estate planning concepts.

Assuming that a decedent does have a will, here is how probate typically proceeds:

The length of a probate can vary depending on many factors, including the size of the estate, state laws, and whether the will is deemed invalid or contested.

In some cases, avoiding probate altogether can cut down on the amount of time it takes to wind up a deceased person's affairs. There are also other reasons to avoid probate, such as keeping probate filings out of the public record and saving money on court costs and filing fees.

Beneficiary designations, joint ownership, trusts, and affidavits are common ways to avoid probate, but only if they are done correctly. Here are some examples of these probate-avoidance tools in action:

Filing a will with the probate court and opening probate are separate actions. A will can be filed whether or not probate is needed. Remember that probate is needed only under certain circumstances, such as when the decedent passed away while owning probate assets. Further, not only can a will be filed with the court when a probate is not needed, some state laws actually require it. Some state laws require the person who has possession of a decedent's will to file it with the court within a reasonable time or a specified time after the date of the decedent's death. The consequences for failing to file a will vary by state but may include being held in contempt of court or payment of fines. Additionally, the person in possession of a will might also be subject to litigation by heirs who stand to benefit from the estate under the terms of the will. The latter also applies if the will-holder files a will but does not file for probate. Failing to file for probate (when probate is necessary) prevents inheritances from being properly distributed.

These legal consequences are usually imposed only on a will-holder who willfully refuses to file a will. If someone you love has passed away and you have their will in your possession, we recommend that you work with an experienced probate attorney who can assist you in determining whether a probate must be opened and whether the will needs to be filed.

Probate avoidance may be one of your goals when creating an estate plan. You should also consider implementing tools in your estate plan to minimize issues that may arise if your estate does require probate.

Your will may have been written years ago and might not reflect current circumstances. You could have acquired significant new accounts or property, experienced a birth or death in the family, left instructions that are vague or generic, or chosen an executor who is no longer fit to serve. An outdated or unclear will can spell trouble when it is time to probate your estate, making it important to identify—and address—issues that could lead to problems, including will contests and disputes.

It is recommended that you update and review your estate plan every three to five years or whenever there is a significant life change or a change in federal or state law. You cannot be too careful when stating your final wishes. For help drafting an airtight will that avoids possible complications, please contact us.

2022-07-25 by Sasha Hartzell

Despite the fact that it happens to every single one of us and is as every bit as natural as birth, very few among us are properly prepared for death—whether our own death or the death of a loved one.

Yet the pandemic might be changing this.

According to Census figures, the pandemic caused the U.S. death rate to spike by nearly 20% between 2019 and 2020, the largest increase in American mortality in 100 years. More than two years and 1 million deaths later, it's more clear than ever that death is not only ever-present, but a central and inevitable part of all our lives.

Graph from the United States Census BureauSome in the end-of-life industry believe that the pandemic's massive loss of life has created an opportunity to transform the way we interact with death, grief, and all of the other issues that arise with the loss of a loved one. Seizing the moment, one startup recently launched Empathy, an AI-based platform designed to help families navigate the death of a loved one. "We're on a mission to change the way the world deals with loss," reads Empathy's 'About Us' page. The company's CEA and Co-Founder, Ron Gura echoes this sentiment:

"For far too many, COVID-19 has been a terrible reminder that death and loss are all around us. But it also represents an opportunity to shift public perception, to bring a topic that has been for far too long shrouded in darkness into the light of day, where we can fully examine it and figure out how best to help those who have to shoulder its burdens."

- Ron Gura, Co-Founder of Empathy

The death of a loved one generates a cascade of emotional, logistical, and financial challenges for those left behind. To further shed light on just how vastly unprepared most of us are when dealing with death, in March 2022 Empathy released its first-ever Cost of Dying Report. In partnership with Goldman Sachs, Empathy's report surveyed more than 2,000 Americans—each of whom had lost a loved one in the last five years—to get a clearer picture of dying's true cost to families.

The report looked not only at the financial burden dying brings, but also at the cost in time, stress, harmed productivity, and strained interpersonal bonds. Complete with insights from advisors, partners, and experts in bereavement, the Cost of Dying Report "bust open the taboo that has for too long kept it out of the public consciousness," said Gula.

Empathy found that the average total bill of death is $12,702. The average cost of a funeral was $7,267—according to the National Funeral Directors Association, that cost has risen 7.6% in the last 5 years. On top of the funeral, families paid an average of $5,846 to hire additional professionals such as lawyers, financial advisors, therapists, and realtors.

Excerpt from The Cost of Dying Report by Empathy

Excerpt from The Cost of Dying Report by Empathy

The average cost of lawyers fee's following the death of a loved one was $3,910. This amount, however, is nearly doubled for estates that required the court process of probate, as was the case for one-third of families surveyed; the average total cost to complete probate for the families surveyed was $16,800.

Beyond the purely financial, The Cost of Dying Report found that families spent 13-20 months completing end-of-life tasks for their deceased loved ones. Study participants clocked an average of 420 hours of work to handle an estate with around five phone calls a week (26 hours per month on the phone!) The majority of families also said it took longer to much longer than expected to wrap up all of the necessary tasks.

In the words of contributing attorney Avi Z. Kestenbaum, "every estate is settled eventually. Even the most complex one. But it is very often a long road to get there—and if you think you know how long, you probably don't."

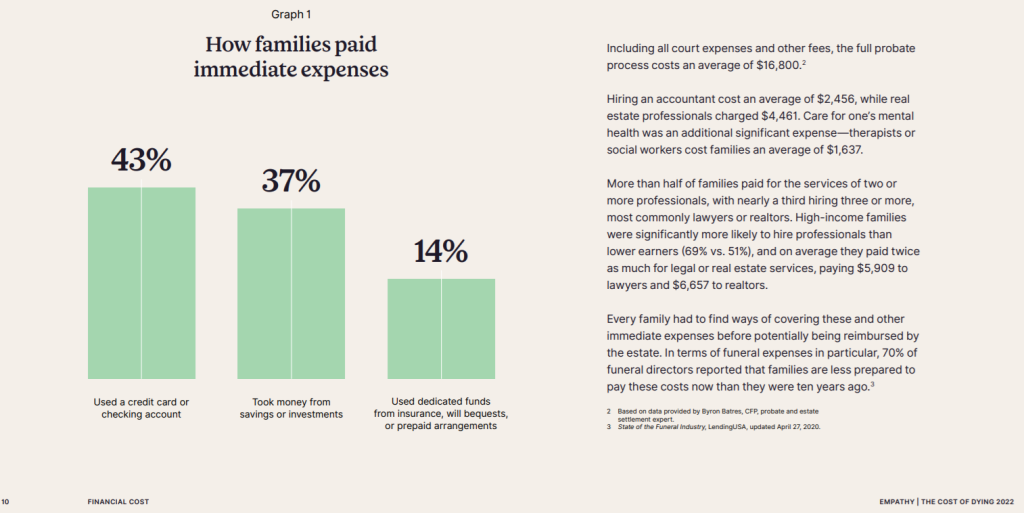

So how do families cover all of these expenses? Unfortunately, the report found that only one in seven families had the costs associated with their loved ones' death prepaid, or were able to use inherited funds. Additionally, more than 50% of families had to deal with estates that included debt. To foot the bill for these expenses, 36.1% of respondents used their own savings or investments, while 42.4% used their checking accounts or credit cards.

For most families, the financial costs associated with loss were exacerbated by a lack of information about exactly how much money they should expect to spend, according to physician Shoshana Ungerleider, MD, in the report's section on death's financial cost. Compounding that stress, Ungerleider says, was the families' fear of making a mistake that will make their financial burden even worse.

"A majority of families find themselves unprepared for and under-informed about the real financial costs of death, with few available resources for finding out," writes Ungerleider. "They can spend months or years terrified that a wrong move will wipe out their inheritance or even their own savings."

As an example of what such a mistake might look like, Ungerleider notes that a lack of proper estate planning can lead to the deceased's home being seized after death for Medicaid Recovery, even if the family member who was their primary caregiver is still living in the home.

Fortunately, there are ways you can dramatically reduce the financial, logistical, and emotional burden for your loved ones upon your death. There are strategies to help your family to avoid the time, expense, and emotional burden associated with probate, such as by placing assets in a properly created and maintained revocable living trust. We also offer planning strategies that can help you and/or your senior parents qualify for Medicaid and other benefits, without putting the family home or other assets at risk.

Our end-of-life planning also includes asset protection, avoiding family conflict, funding long-term care, and estate tax mitigation, just to name a few. Sit down with us for a Family Wealth Planning Session to find the most effective and affordable planning solutions for you and your family.

The more you prepare for your own eventual death and learn about the process, the more support you can offer friends and family members who have recently lost a loved one. As Kestenbaum notes, "as a society, then, we can be much more aware not only of the stress that our bereaved friends, neighbors, coworkers, or employees are under, but also understand that the pressure will persist for a very long time. So even one year later, try to ask: How are you? Is there anything I can do to help? That will be very meaningful."